Financial planning is often perceived as a purely rational and analytical process. However, emotions play a significant role in shaping financial behaviors and decisions, sometimes more than logic itself. Understanding the influence of emotions on financial planning is crucial for both individual investors and financial advisors aiming to craft effective strategies that balance analytical insights with psychological factors. This article explores the intricate relationship between emotions and financial decision-making, highlighting practical examples, common emotional pitfalls, and future trends in emotionally intelligent financial planning.

Emotional Dynamics in Financial Decision-Making

When people engage in financial planning, their emotions inevitably intertwine with logic. Fear, greed, anxiety, and hope are common emotions that influence investment choices, budgeting practices, and risk tolerance. Studies show that emotional bias can lead to overtrading, panic selling, or overly conservative approaches that limit growth potential. For example, during the 2008 financial crisis, many investors reacted emotionally to the volatile markets, selling off assets at significant losses due to panic, only to miss out on the subsequent market recovery.

Emotions also affect daily financial habits such as spending, saving, and debt management. According to a survey conducted by the American Psychological Association in 2022, 72% of Americans reported feeling stressed about money, which correlates with impulsive spending or avoidance of financial planning altogether. Emotional awareness, therefore, is vital for maintaining a balanced financial approach that supports long-term goals rather than short-term emotional satisfaction.

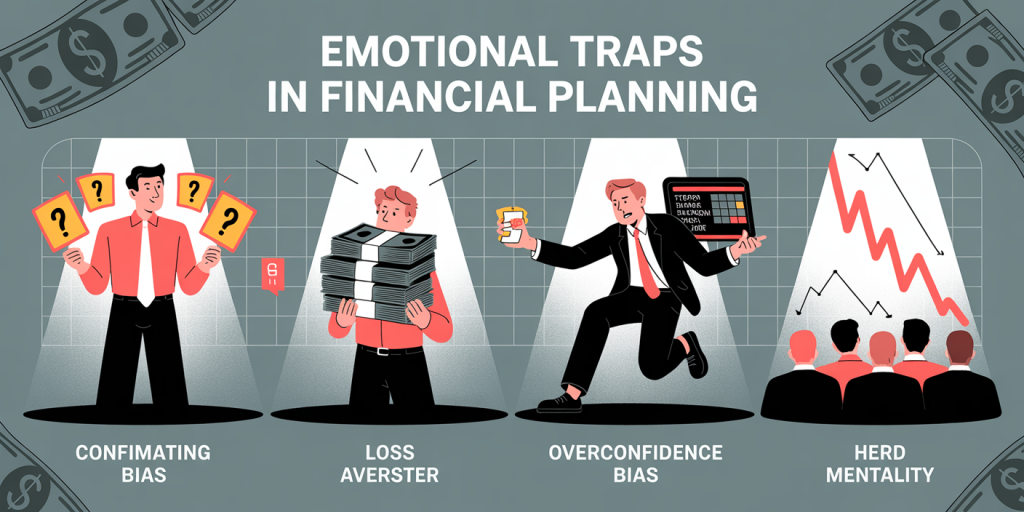

Common Emotional Traps in Financial Planning

Emotional biases can undermine even the most carefully drafted financial plans. One of the most notable emotional traps is confirmation bias – the tendency to seek information that confirms existing beliefs while dismissing contradictory evidence. This bias can cause investors to hold onto failing investments, convinced they will rebound despite clear indicators to the contrary. A practical example is the prolonged holding of tech stocks during the dot-com bubble collapse in the early 2000s, where emotional attachment to optimistic forecasts clouded judgment.

Another prevalent emotional trap is loss aversion. Behavioral economists Daniel Kahneman and Amos Tversky describe loss aversion as the tendency to prefer avoiding losses over acquiring equivalent gains. This can lead investors to make overly cautious decisions, avoiding opportunities for growth due to fear of short-term losses. For example, retirees often keep excessive cash reserves with low returns, driven by a fear of losing their nest egg, which may actually diminish their purchasing power through inflation.

| Emotional Trap | Description | Financial Impact | Example |

|---|---|---|---|

| Confirmation Bias | Seeking information that confirms beliefs | Holding losing investments too long | Dot-com bubble stocks |

| Loss Aversion | Preferring to avoid losses over securing gains | Overly conservative investment | Retirees keeping excessive cash |

| Overconfidence Bias | Overestimating one’s knowledge or predictive ability | Excessive trading and risk-taking | Frequent buying and selling |

| Herd Mentality | Following the crowd regardless of own judgment | Market bubbles and crashes | 2008 housing market collapse |

These emotional pitfalls are common but manageable through awareness, education, and behavioral discipline.

The Interplay of Emotional Intelligence and Financial Planning

Emotional intelligence (EI) involves recognizing, understanding, and managing one’s own emotions as well as empathizing with others’ feelings. In financial planning, high EI facilitates better decision-making by allowing investors and advisors to separate emotion from logic and respond appropriately to financial challenges. For instance, a financially literate individual with high EI may recognize feelings of anxiety during a market downturn but refrain from panic selling, instead focusing on long-term strategy.

Financial advisors increasingly integrate emotional intelligence into client interactions, fostering trust and reducing emotional bias in decision-making. According to a study published in the *Journal of Behavioral Finance* (2021), advisors who employ emotionally intelligent practices see a 25% increase in client satisfaction and improved adherence to financial plans. Emotional coaching helps clients set realistic expectations, manage stress, and maintain perspective during market volatility.

Consider the case of Jane, a middle-aged professional approaching retirement. Her advisor noticed heightened anxiety during market dips and introduced mindfulness techniques alongside portfolio adjustments to reduce volatility exposure. Over time, Jane became more confident and less reactive, resulting in more stable financial progress.

Cultural and Societal Influences on Financial Emotions

Financial emotions are not experienced uniformly across cultures and societies. Social norms, cultural values, and economic environments shape how people perceive money and make financial decisions. In collectivist societies, for example, there can be a stronger emotional emphasis on familial financial obligations, which affects saving and borrowing behaviors differently than in individualistic societies.

A comparative study by the World Bank (2023) highlights differences in financial anxiety levels, with respondents in higher-income countries reporting lower stress related to short-term cash flow, but increased concern about long-term retirement preparedness. In contrast, emerging economies show higher immediate financial stress due to income volatility, which leads to aggressive self-protective financial actions such as hoarding cash or avoiding credit altogether, sometimes at the expense of potential investment gains.

| Region | Dominant Financial Emotions | Financial Behavior Patterns | Economic Impact |

|---|---|---|---|

| North America | Market anxiety, optimism | Active investing, retirement savings | Growth-oriented portfolios |

| East Asia | Familial responsibility, caution | Preference for savings, low risk | High savings rates, low debt |

| Sub-Saharan Africa | Survival stress, distrust | Cash hoarding, informal financial practices | Limited portfolio diversification |

Understanding these cultural dimensions helps financial planners design more empathetic and effective plans that resonate with clients’ emotional realities.

Practical Strategies to Manage Emotions in Financial Planning

To mitigate emotional biases and improve financial outcomes, investors and planners can adopt several practical strategies. First, establishing clear, measurable financial goals reduces ambiguity and emotional reaction to market fluctuations. Goal-setting anchors decisions to long-term objectives rather than short-term feelings. For example, systematically automating retirement contributions removes emotional interference from saving discipline.

Second, diversification of investments acts as a buffer against emotional responses to specific asset performance. A well-diversified portfolio can lower anxiety by reducing the impact of volatility in any single investment. The principle of “don’t put all your eggs in one basket” is emotional wisdom translated into financial practice.

Third, regular financial reviews with a trusted advisor can provide objective perspectives during emotionally charged times. Together, clients and advisors can revisit risk tolerance levels, assess progress, and adjust strategies sensibly. Behavioral coaching that incorporates emotional awareness can further reinforce disciplined adherence to plans.

An example illustrating these strategies comes from the case of a millennial investor, Michael, who initially reacted impulsively to cryptocurrency market swings. Upon engaging a financial advisor, Michael implemented automated monthly investments in a diversified fund, committed to quarterly reviews, and learned mindfulness techniques to manage emotional impulses. Over three years, this approach stabilized his portfolio growth and reduced stress.

Future Perspectives on Emotionally Aware Financial Planning

As technology and behavioral science converge, the future of financial planning will increasingly incorporate emotional analytics and personalized emotional support. Artificial intelligence tools can detect emotional states via communication cues, enabling advisors to respond empathetically and tailor advice accordingly. Early developments in fintech include apps that track mood linked to market interactions, alerting users when emotional biases may be influencing decisions.

Moreover, integrating neuroscience into financial planning education will help clients understand how the brain processes risk and reward, paving the way for more informed choices. Educational programs that combine financial literacy with emotional management skills are emerging as vital components of holistic financial wellness.

Additionally, societal shifts towards valuing mental health and well-being suggest that future financial services will prioritize emotional resilience alongside fiscal security. Holistic financial wellness programs that address stress, financial trauma, and emotional drivers will become mainstream, supported by interdisciplinary teams including psychologists and financial planners.

In conclusion, recognizing and addressing the role of emotions in financial planning is essential for achieving sustainable financial success. Emotional intelligence, cultural sensitivity, and practical behavioral strategies enable individuals and advisors to navigate the complex interplay between feelings and finances effectively. With ongoing advancements in technology and behavioral insights, the next frontier of financial planning promises a more emotionally informed, empathic, and successful approach to managing money.

Deixe um comentário