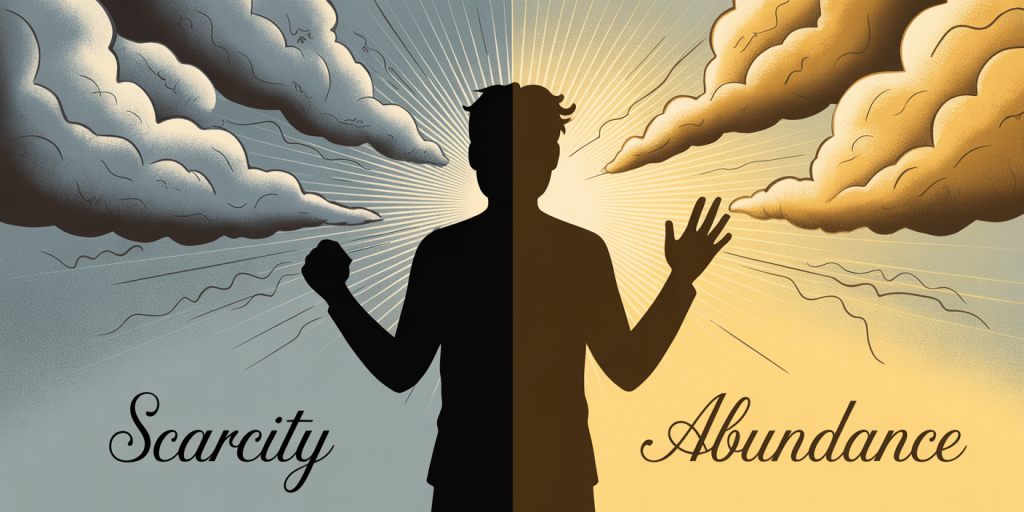

In the ever-evolving landscape of personal finance, the mindset individuals adopt toward money can significantly influence their financial stability and growth. Two dominant psychological approaches frequently debated by financial experts and behavioral economists are the scarcity mindset and the abundance mindset. These mental frameworks are not merely abstract concepts; they actively shape economic decision-making, risk tolerance, and wealth accumulation.

Understanding the contrast between a scarcity mindset—where resources are perceived as limited—and an abundance mindset—where opportunities and resources are seen as plentiful—can provide crucial insights into effective money management. The implications of these mindsets extend far beyond personal accounts, affecting spending habits, investment strategies, and even interpersonal financial relationships.

Defining Scarcity Mindset and Abundance Mindset in Financial Contexts

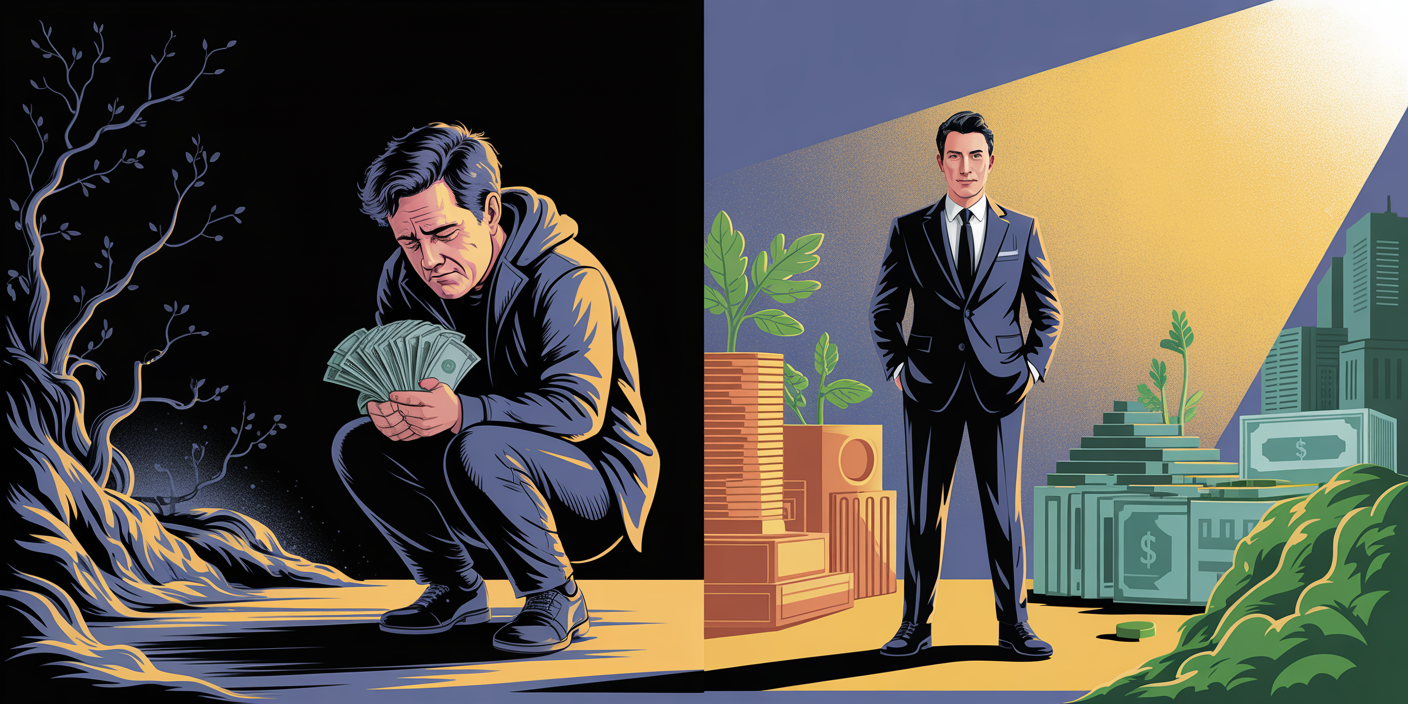

A scarcity mindset in money management is characterized by a persistent fear that there is never enough money to meet needs or desires. This perception often leads to overly cautious financial behavior, such as under-spending, hoarding cash, and avoiding investments due to fear of loss. Psychologically, scarcity mindset reinforces stress and anxiety around financial decisions, resulting in limited economic growth over time.

For example, individuals holding a scarcity mindset might avoid investing in the stock market due to the perception that investing is risky and may lead to losing what little money they have. According to a 2022 survey by Bankrate, approximately 37% of American adults reported having less than $1,000 in savings, and many expressed a hesitation to invest, illustrating the scarcity-driven tendency to prioritize immediate security over long-term wealth creation.

Conversely, an abundance mindset embraces the belief that money and opportunities are plentiful. People with this mindset tend to focus on expanding their financial horizons, engaging in investments, seeking multiple income streams, and maintaining a positive outlook on their capacity to improve financial well-being. This mindset fosters optimism and proactive behavior that often lead to better economic outcomes.

An abundance mindset does not imply reckless spending. Instead, it encourages strategic and confident financial management that balances saving and investing with calculated risks to increase assets. Jeff Bezos, founder of Amazon, has often highlighted how his abundance mindset fueled his willingness to invest heavily in the future, famously stating that he viewed money as a “tool to build and innovate” rather than something to hoard.

Behavioral Impacts on Spending and Saving Patterns

The scarcity mindset typically leads to conservative financial habits, where spending is minimized, sometimes excessively, and saving is prioritized above all else. This behavior may result in missed opportunities for wealth generation. For example, an individual might avoid purchasing a reliable used car to save money, ultimately spending more on repairs for an old vehicle, reflecting the shortsightedness caused by scarcity-oriented thinking.

On the other hand, those with an abundance mindset often display balanced spending and saving behaviors. They allocate funds not only to emergency savings but also to investments, personal growth, and experiences that can yield long-term returns. A study by the University of California (2023) found that people who identified with an abundance mindset were 35% more likely to participate in employer-sponsored retirement plans compared to scarcity-minded individuals.

The following table illustrates typical spending and saving traits associated with each mindset:

| Aspect | Scarcity Mindset | Abundance Mindset |

|---|---|---|

| Spending tendencies | Extremely cautious, often frugal | Balanced, focused on value and growth |

| Saving habits | Prioritizes cash accumulation | Saves and invests strategically |

| Risk tolerance | Low, avoids financial risks | Moderate to high, embraces calculated risks |

| Financial stress | High, constant worry about insufficient funds | Lower, confidence in financial future |

| Long-term planning | Short-term focus, reactive | Proactive, goal-oriented |

Effects on Investment Behavior and Financial Growth

Investment decisions are profoundly influenced by whether one adopts a scarcity or abundance mindset. Scarcity-minded individuals often view investments as gambling or risks threatening their limited financial resources. Consequently, they may avoid diversification or high-growth assets, leading to stagnant asset portfolios.

Consider the case of retirees who avoid stock market investments due to fear of losing principal funds. While safer bonds and fixed deposits provide stability, over-reliance on these conservative instruments in low-interest environments may erode purchasing power. Data from Fidelity Investments (2023) indicate that retirees who maintain a diversified portfolio including equities tend to outpace inflation by 1.5 times, improving their quality of life in later years.

By contrast, abundance-minded investors see financial markets as opportunities to multiply wealth over time. They educate themselves on market trends, seek advice from professionals, and embrace long-term investment horizons. Warren Buffett’s wealth trajectory exemplifies the success of an abundance mindset, which emphasizes patience and calculated risk-taking, resulting in sustained financial growth.

Impact on Psychological Well-being and Money Management

The scarcity mindset is often associated with increased financial stress, anxiety, and even decision paralysis. This mental state triggers the brain’s survival mode, narrowing focus strictly to short-term survival over long-term planning. A report from the American Psychological Association (2023) found that financial stress is a leading cause of mental health issues, with scarcity thinking contributing significantly to this phenomenon.

In contrast, an abundance mindset helps foster psychological resilience and reduces the emotional burden related to money. Individuals adopting this mindset are more likely to engage in positive self-talk, maintain financial discipline, and communicate openly about money matters. These behaviors promote healthier relationships and reduced stress, critical components of overall well-being.

Practical Strategies for Transitioning Toward an Abundance Mindset

Transitioning from a scarcity to an abundance mindset requires intentional effort and consistent practice. One effective method is financial education that shifts perception from fear to knowledge. For instance, workshops on budgeting, investment basics, and debt management empower individuals with the tools needed to take control of their finances confidently.

Another practical approach is goal-setting that focuses on long-term vision rather than immediate scarcity fears. By establishing clear financial goals—such as retirement, education, or homeownership—individuals can align their spending and saving habits with an abundance-oriented framework.

Mindfulness and gratitude exercises have also shown to reduce scarcity-driven financial anxiety. Research from Stanford University’s Center for Compassion and Altruism Research (2022) demonstrates that practicing gratitude increases mental bandwidth for complex decision-making, facilitating smarter financial choices.

Looking Ahead: How Changing Mindsets Could Shape Future Financial Landscapes

As digital financial tools and platforms democratize wealth-building opportunities, the abundance mindset is poised to become increasingly relevant. For example, fractional investing platforms like Robinhood and Acorns have made market participation accessible to millions, encouraging users to adopt a more optimistic approach to growing personal wealth.

Furthermore, emerging trends such as financial literacy programs integrated into school curriculums worldwide aim to nurture abundance mindsets from early ages. A 2024 OECD report highlights that countries with mandatory financial education see 20% better saving rates among young adults, underlining the importance of mindset cultivation.

Technological advances in artificial intelligence and algorithm-driven financial advisors will also empower individuals to manage money more efficiently, potentially reducing fears and limitations associated with scarcity thinking. With better data and automated strategies at their disposal, consumers can execute more confident financial plans.

However, obstacles remain. Economic inequalities and systemic barriers continue to fuel scarcity perceptions among disadvantaged groups. Addressing these challenges requires policy interventions that ensure equitable access to resources, enabling more people to embrace an abundance mindset and build sustainable financial futures.

—

References: Bankrate, “Trends in American Savings,” 2022. University of California Behavioral Finance Study, 2023. Fidelity Investments Retirement Insights, 2023. American Psychological Association, “Financial Stress and Mental Health,” 2023. Stanford University Center for Compassion and Altruism Research, 2022. OECD, “Financial Literacy and Youth Saving Rates,” 2024.

Deixe um comentário